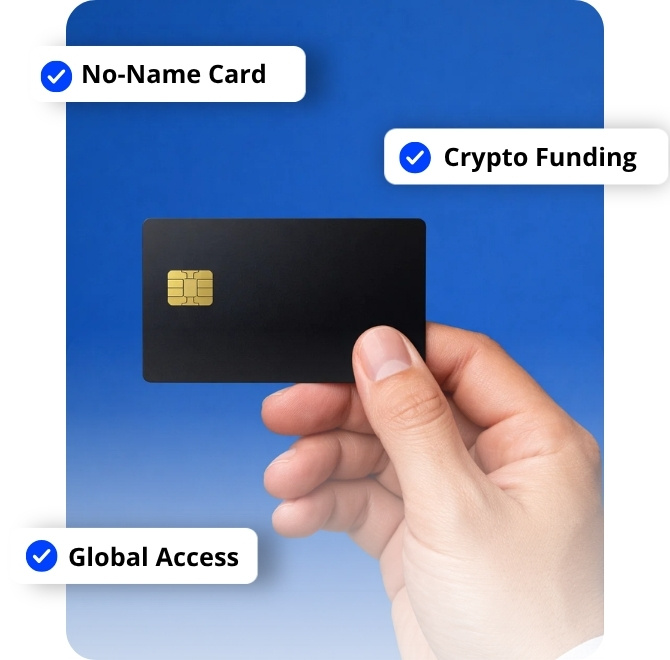

An anonymous offshore card is a prepaid debit card issued in a non-CRS jurisdiction with no name printed on the front of the card. It is designed for clients who want practical spending privacy, easier crypto-to-fiat use, and a more discreet way to manage everyday international expenses. An anonymous offshore prepaid card is not a tool for hiding from the law; it is a lawful privacy solution for people who want their spending and card usage kept out of unnecessary public visibility.

Excellent 4,6 out of 5

An anonymous offshore card combines everyday payment functionality with a stronger privacy profile, giving clients a practical way to spend internationally without unnecessary exposure.

An anonymous offshore card gives you the functionality of a normal prepaid debit card, but with a different privacy profile. The card does not display the holder’s name on the face of the card, and the card is issued through an offshore jurisdiction that does not automatically exchange card data under CRS. Your identity is still known to the issuer through KYC, but it is not printed on the card and is not automatically transmitted through no-CRS reporting channels.

This type of card is designed for internationally active clients who value flexible spending, crypto compatibility, and a higher level of privacy in everyday payments.

This is where an anonymous debit card offshore setup or an offshore card no-name format becomes especially attractive: it gives the user functional payment access without turning the card itself into a personal name tag.

The core value of an anonymous offshore card lies in practical privacy, flexible funding, and international usability rather than in empty marketing myths.

A true no-name card does not show your personal name on the front. This gives an additional layer of privacy in everyday use and reduces casual exposure during payments or travel.

The card is issued in a jurisdiction outside automatic CRS exchange. That means there is no automatic transmission of card balance and transaction data to your home tax authority through CRS. You still remain responsible for tax compliance in your country of residence.

A crypto offshore card can be funded through USDT, USDC, BTC, or wire transfer, depending on the card program. This makes it easier to convert digital wealth into usable purchasing power without unnecessary complexity.

An anonymous prepaid debit card can support higher merchant spending and ATM usage than many mass-market prepaid products. Exact limits depend on the program, but the structure is designed for serious practical use, not just souvenir-level spending.

Cards can be shipped through express courier with worldwide delivery in many cases. That makes the product useful for international clients who need a working solution quickly and without an office visit.

If the card is lost, stolen, or compromised, it can be blocked and replaced. The prepaid balance remains tied to the program, not to the physical plastic itself, which is one of the reasons a prepaid offshore card no-name format is often preferred for travel and mobile use.

An anonymous offshore card and an offshore bank account solve different problems. One is primarily a spending tool; the other is a full banking relationship for holding and moving larger assets. In practice, many clients use them together rather than choosing one over the other.

Use the card for private day-to-day spending, travel, online payments, and crypto-linked liquidity. An offshore anonymous card is often the fast-access layer.

Use the bank account for wealth management, larger balances, and long-term international structuring. The bank account is the deeper storage layer.

If you need help comparing cards, payment options, delivery routes, or related offshore banking solutions, speak with our team for a confidential review of your case. We help clients choose the right card format, understand KYC requirements, and avoid mismatches before ordering.

Contact an ExpertUliana Syva

Consultant for company registration, bank account opening, residency, and citizenship.

1000+

successful cases

13+

years of experience

The ordering process is straightforward, fully remote, and designed to balance privacy with proper issuer compliance. Ordering an anonymous offshore card is more straightforward than many clients expect. The process is remote, structured, and designed to balance privacy with issuer compliance.

We review your spending profile, preferred funding method, delivery country, and network preference, such as UnionPay, Visa, or Mastercard.

We help you choose the best card option for your needs. In some cases, a combo package with two cards linked to one prepaid balance may be available.

You submit a light compliance package to the issuer: passport copy, proof of address, and a source of funds declaration. Everything is handled remotely.

Once approved, the card is dispatched through international courier, usually within 24–48 hours from stock, depending on program availability.

You activate the card according to the program instructions and fund it via crypto or wire transfer. After activation, the card is ready for spending, ATM use, and international transactions.

KYC does not cancel privacy; it simply means the issuer must know who you are, while your personal data remains protected within the card program.

Every serious financial product involves KYC. The word “anonymous” here does not mean “no documents at all.” It means that your card is issued in a privacy-oriented structure where your name is not displayed on the plastic and where data is not automatically reported under CRS.

Typical documents include:

Certified or notarized copy of passport, national ID, or driver’s license

Proof of residential address dated within the last 3 months

Source of Funds Declaration explaining how the money used to fund the card was earned

In some cases, a bank reference letter or additional compliance documents

Source of Funds explains where the loaded money comes from: salary, business income, sale of assets, investments, crypto profits, inheritance, or another lawful source. Issuers request it because AML and compliance rules require them to understand the origin of funds before they activate a card program.

Clients usually want clear answers on limits, loading methods, and costs before they order, and this block is where those practical details matter most.

Typical programs offer higher spending and withdrawal limits than standard consumer prepaid cards. Final figures depend on the issuer and the selected card tier. If higher aggregate volume is needed, a combo pack with two linked cards can sometimes provide more flexibility.

Funding options may include USDT, USDC, BTC, wire transfer, or transfers from another approved source. Timing depends on the network and payment route, but crypto-friendly loading is one of the key advantages of this type of card.

The fee structure usually includes the cost of the card itself, loading fees, ATM withdrawal fees, courier delivery costs, and sometimes a monthly maintenance fee. We clarify all charges before the order is placed, so there are no surprise commissions jumping out of the bushes later.

The right provider does more than sell a card — it helps match the product to your privacy goals, compliance profile, and international usage needs. Choosing the best anonymous offshore prepaid card is not about ordering random plastic online. It is about matching the card program to your profile, your privacy goals, and your funding logic.

We do not offer one generic card to everyone. The recommendation depends on spending volume, preferred funding source, delivery country, and network preference.

We have long-standing experience in offshore banking, privacy-oriented financial solutions, and cross-border structuring for international clients.

Client information is handled with strict confidentiality. Your documents are used for issuer compliance, not for casual circulation.

All costs are explained before you commit. No hidden fees, no mystery deductions, and no charming surprises after payment.

An anonymous offshore prepaid card is a fast, lawful, and effective tool for financial privacy, crypto spending, and international mobility. It gives you a no-name prepaid format, crypto-friendly funding, non-CRS issuing logic, and worldwide delivery without forcing you into a full offshore banking setup on day one. Contact us today for a confidential consultation, and we will help you choose the right card for your needs.

Yes, in the sense of privacy and limited exposure, not in the sense of “the issuer knows nothing.” The issuer still performs KYC, but your name is not printed on the card, and the program is structured to avoid automatic CRS reporting.

In most cases, yes. It is a lawful financial product. You remain responsible for complying with tax and reporting obligations in your country of residence.

The main differences are jurisdiction, privacy profile, no-name format, crypto-friendly funding options, and non-CRS issuing logic. A regular prepaid card usually does not offer this combination.

The process is simple: consultation, card selection, KYC, payment, shipping, activation, and funding. We guide clients through each stage.

Cards are usually dispatched within 24–48 hours from stock after approval. Delivery time depends on the destination country and courier route.

Yes, some programs support combo packages with two or more cards linked to the same prepaid balance. This can be useful for higher aggregate usage or backup access.

Yes. Most programs support ATM withdrawals internationally, subject to network support and program limits. Exact ATM limits depend on the card type.

Yes. Many programs support funding through USDT, USDC, BTC, and bank transfer. The crypto is converted into fiat spending capacity according to the issuer’s rules.

That depends on the selected card program. Limits usually apply to single merchant transactions, daily ATM withdrawals, and maximum stored balance. Exact figures are confirmed during consultation.

If the card is issued through a non-CRS prepaid card program, there is no automatic CRS reporting from the issuing jurisdiction. That said, the client remains responsible for their own tax reporting duties at home.